The RBI hedging support has boosted FCNR(B) deposit rates, but slowing NRI incomes may limit inflows, raising questions about income versus interest rate effects.

Syllabus Areas:

GS III - Economy

The Reserve Bank of India (RBI) has decided to bear full hedging cost till Sept 30, 2026 to banks for raising fresh 3–5 year FCNR(B) deposits.

-

This made banks to be euphoric about mobilization of FCNR(B) deposits.

-

Hence banks to offer higher rates for such deposits varying between 6 and 7.1%.

-

Hence the opportunity to convert NR(E)RA deposits to FCNR(B) deposits.

Hedging cost: Hedging cost is the expense incurred to protect against adverse movements in exchange rates, interest rates, or prices by using financial instruments such as forwards, futures, options, or swaps.

What is an FCNR(B) Deposit?

FCNR(B) stands for Foreign Currency Non-Resident (Bank) Deposit.

The deposit remains in the foreign currency itself.

Example

If an NRI deposits:

-

$10,000 in an FCNR(B) account

The account continues to remain in dollars.

After maturity:

-

Principal + Interest are paid in dollars.

Even if the Rupee depreciates or appreciates, the depositor is unaffected.

Therefore, exchange rate risk is eliminated for the depositor.

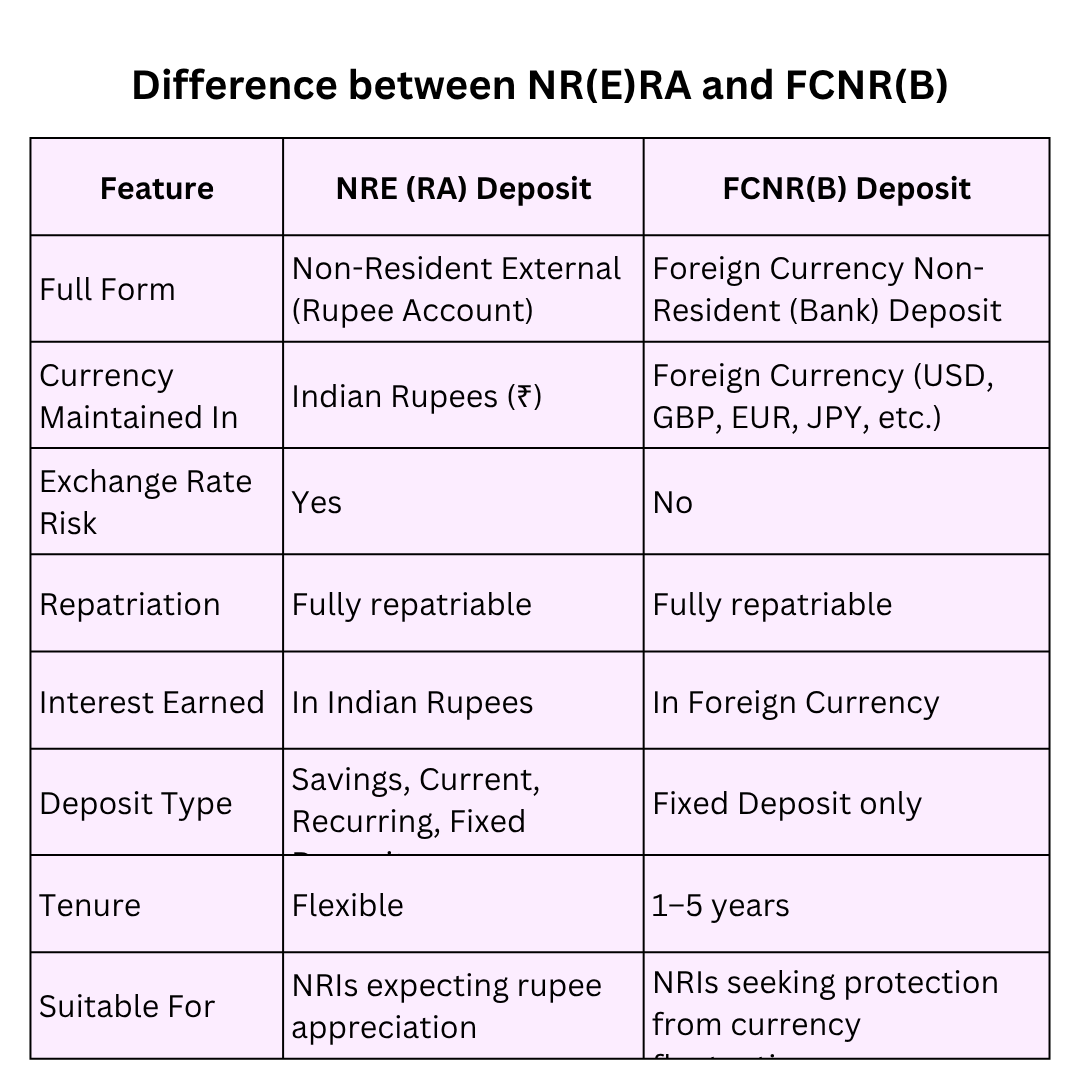

Difference Between NRE (RA) Deposits and FCNR(B) Deposits

Many NRIs keep their savings in India through either NRE Accounts or FCNR(B) Deposits. Though both are meant for Non-Resident Indians, they differ significantly.

Understanding Savings Behaviour

Economists generally identify two major determinants of savings:

1. Income

Higher income enables households to save a larger portion of their earnings.

2. Rate of Interest

Higher interest rates provide incentives to save rather than consume.

The success of RBI's initiative depends on which factor exerts a stronger influence on NRI depositors.

-

The US is the topmost source of remittances to India, accounting for 27.7% of India's total inward remittances.

-

Further, the retail Indian depositors constitute the major providers of FCNR(B) deposits in dollars.

-

The retail Indian depositors in the US mainly comprise:

-

H1-B workers

-

Green Card holders

-

OPT (Optional Practical Training) interns

Remittances:

Remittances are funds transferred by individuals working abroad to their families or dependents in their home country, providing financial support and contributing significantly to household income and economic development.

The Trump Factor and Its Economic Impact

Despite attractive interest rates, developments in the US labour market can influence NRI savings behaviour.

Changes in immigration policies and employment conditions during Donald Trump's administration led to:

-

Job uncertainty among foreign workers.

-

Reduced employment opportunities in some sectors.

-

Income losses for certain categories of Indian professionals.

-

Some workers returning to India or shifting to lower-paying jobs.

This highlights an important economic reality:

Savings depend not only on interest rates but also on income levels.

Even if deposit rates increase, lower incomes may reduce the ability of NRIs to save.

-

Hence, the outstanding FCNR(B) deposits (in dollar) grew by just 2.9% as against:

-

27.5% in 2024–25

-

32.9% in 2025–26

-

Therefore, will the income effect overshadow the interest rate effect?

-

If so, then banks may have to focus on bulk FCNR(B) deposits from rich or super-rich.

Way Forward

To sustain FCNR(B) inflows, banks may need to:

-

Target high-net-worth NRIs.

-

Mobilize bulk FCNR(B) deposits from wealthy investors.

-

Offer innovative deposit products.

-

Improve digital banking services for overseas Indians.

-

Diversify deposit sources beyond the United States.

At the policy level, maintaining macroeconomic stability and ensuring attractive returns on foreign currency deposits will remain crucial.

The RBI's decision to absorb hedging costs has undoubtedly increased the attractiveness of FCNR(B) deposits by enabling banks to offer higher interest rates.