India is the world’s second-largest steel producer. Steel has an output multiplier effect of 1.4x on GDP and an employment multiplier factor of 6.8x. For every ₹1 increase in steel production, GDP grows by ₹1.4, and for every job created in the steel sector, 6.8 additional jobs are generated in related industries.

Challenges:

- Sluggish demand and gaps in capacity utilization.

- Per capita steel usage is progressing slowly, and infrastructure projects need a stronger push.

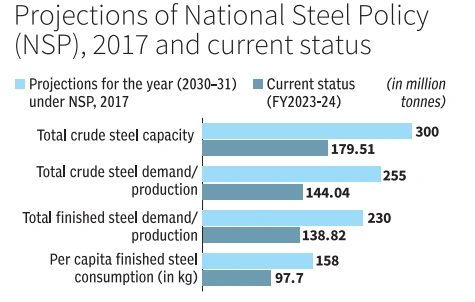

- The sector requires a CAGR of 7.61% annually from 2023-24 to 2030-31 to meet the target of 300 million tonnes of crude steel capacity.

- A shortfall of 120.49 million tonnes in crude steel capacity and 110.96 million tonnes in crude steel demand/production needs to be addressed.

Government Initiatives:

- The National Steel Policy (NSP) 2017 sets ambitious targets for the steel industry.

- The government reduced the basic customs duty on ferro nickel and extended the duty exemption on ferrous scrap until March 2026.

- The Domestically Manufactured Iron & Steel Products (DMI&SP) policy prioritizes domestically produced steel for government procurement. Innovation and Sustainability:

- Emphasis on eco-friendly production practices to reduce environmental impact and attract global markets focused on green initiatives.

- Expansion of domestic and international markets for finished steel products is crucial.

Global Competitiveness:

- India’s steel output expanded at a 6% CAGR between 2019 and 2023, outpacing China’s 1% growth.

- ASEAN and India are projected to account for nearly 89% of Asia’s steel-making capacity additions.

Private Sector Involvement:

- The private sector has been hesitant to add capacity due to uncertainty regarding growth.

- Large capital investment requirements for setting up and maintaining steel plants have limited new entrants in the sector.